SMALL BUSINESS LOAN PROGRAM

The following is a supplement to Policies & Procedures of NPIC EDC, INC. The policies and procedures herein shall apply in consideration and underwriting loan applications for small business loan program (Program).

The Policies and Procedures outlined hereinafter are to be adhered to by staff and management of NPIC EDC, INC. and members of the independent Credit Committee.

Loan Applications

Loan Applications for borrowing(s) under the Program may be submitted either directly or through loan brokers to NPIC EDC, INC. The borrower must be located within the boundaries of Los Angeles County.

The applicants’ front-end payments for loan Application fee and credit report fee are non-refundable.

The form of the Loan Application, and Data Request Check List are attached hereto.

Secured Term Loan(s)

The Program offers secured term loans of three (3) to ten (10) years, each loan in the amount of not less than $150,000 and up to $950,000, to qualified businesses.

The Program is not designed to offer revolving lines of credit.

Job Creation Commitment

The sole policy objective of the Program is for the borrowers under this Program to commit to creation of new permanent full time equivalent (FTE) jobs.

The minimum requirement from each borrower is to commit to the creation of one FTE job per $50,000 of the loan received. In addition, 51 percent of the FTE jobs must be filled in, or made available to, low and moderate-income persons.

In the course of contract with NPIC EDC, INC., the borrowers must list all job openings at one of the WorkSource Centers administered in the Los Angeles County. The job listings at the WorkSource Centers will evidence the borrower’s making available the new employment opportunities to the unemployed and low and moderate-income persons.

Non-Compete with Private Lenders or SBA

The offering of this Program is not to compete with, or supplant, secured term loans that are offered by banks, SBA or other private financial institutions.

The Program is designed to offer secured term loans only to qualified borrowers with viable loan proposals that are declined by private banks for reasons such as credit crunch.

The Program may not be used for either refinancing or rescuing an otherwise failed business.

Eligible Use of Loan Proceeds

Loan funds may be expended only for uses deemed eligible and appropriate by NPIC EDC, INC.

Complete Loan Applications

Staff at NPIC EDC, INC. will consider financial analysis of only complete applications. All incomplete applications will be returned to the originating source, excluding fees.

Loan Fee

Concurrent with execution of Loan documents, borrower shall pay Loan Fee of up to 2.5 percent, flat, of the loan commitment amount. The Loan Fee may be paid directly by the borrower, or by deduction from the Loan proceeds.

Interest Rate

For the initial 12 months of a Loan commitment, interest rate of the Loan advances will be fixed at then the prevailing yield for 10 Years US Treasury Bonds plus 2.5 percent per annum. The interest rate is subject to annual adjustments, subject to changes in the US Treasury benchmark.

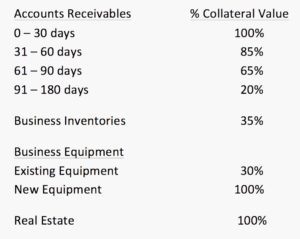

Collateral

Eligible collateral under the Program may be as follows:

Ratio of Loan amount to Collateral Value must not exceed 65 percent.

The value of Business Receivables and Inventories must be (a) certified as to amount and sustainability

(during term of the loan requested) by the applicant, and (b) the amounts must be verifiable in the certified financial statements.

Business Equipment offered as Collateral shall mean qualified depreciable equipment, located within the geographic limits of the Los Angeles County, excluding related tools and fixtures. The eligible business equipment should currently and for the duration of Loan be used by the Borrower to process material or energy for production of end-products. Both the existing and new equipment offered as Collateral must be income producing, where the use of such equipment results in direct-income, and not indirect-income, to the borrower.

Real Estate provided as Collateral must be a commercial and income producing property, and secured by at a minimum second deed of trust. Single-family dwellings will not be considered as a Collateral option. The ratio of aggregate secured encumbrance(s) of the real estate provided as Collateral, including the City Loan, to current market value should not exceed 65 percent.

Except for Real Estate and Business Equipment, borrowers must reaffirm the Collateral Value provided as security for the City Loans on a semi-annual basis. The certification of Collateral Value must be made either business owner or a Certified Public Accountant. The same or alternate Collateral, as defined herein, must replenish any depletion in the Collateral value.

An MAI appraiser must appraise all real estate offered as Collateral for the Loans. The appraisal reports must be current, produced not later than six months from date of applications, and will be subject to further review and verification of the underlying assumptions by NPIC EDC, INC.

Recourse & Guaranty

The Loans shall have full recourse to borrowers. In case the borrowers cannot provide the required recourse, an independent third party guaranty, acceptable at reasonable discretion of NPIC EDC, INC. will be required.

Debt Coverage

In reference to Attachment – B (Cash Flow), all borrowers must demonstrate having debt service ability at coverage ratio of not less than 1.20:1.00.

If a loan proposal relies on cash flow projections, loan application must accompany detailed cash flow projections based on prudent assumptions. The narrative of cash flow assumptions must be clear and consistent. The projections must demonstrate the business’ having debt service ability with coverage ratio of not less than 1.20:1.00.

Credit History

NPIC EDC, INC. will obtain credit reports on all borrowers and guarantors. The borrowers and guarantors’ credit rating will be a factor in recommending the loan applications to Credit Committee.

Time to Reply by NPIC EDC, INC.

NPIC EDC, INC. will reply to all loan applications within ten (10) business days from when applications are received.

Credit Committee

Loan Applications that meet credit, underwriting and regulatory pre-conditions will be recommended by NPIC EDC, INC. to the panel of Credit Committee.

The panel of credit committee will consist of minimum three pre-approved representatives from the credit departments of qualified lending institutions. There shall be no advance lobbying for any of the transactions with the panel members.

EDD will invite participants for periodic Credit Committee meetings, on a rotating basis, subject to the panel members’ availability and consideration of potential conflicts of interest.

Loan Documentation

All loans are to be documented to the satisfaction of the Attorneys of NPIC EDC, INC. Security documents for each and every loan are to be recorded, including the filing of UCCs.

Borrower’s disagreement with terms and conditions of the Loan documents may result in rejecting a Loan Application.

Loan Disbursements

All loan disbursements are subject to borrower’s provision of supporting documentation as reasonably required by NPIC EDC, INC., and subject to test of reasonability and eligibility.

Funding of any disbursement is subject to CDD receipt of funds from sponsors.

Collection Proceeding

Upon a technical or financial default by any of the borrowers, on the expiration of grace period for the borrowers to remedy such defaults, NPIC EDC, INC. will proceed to liquidate the underlying Collateral and pursue all other remedies and recourses against the borrowers and guarantors.

Attachment